Made in China

July 2026 -- Last free letter for a year.

The Rover

Made in China

I spent the weekend of June 20th wiring my garage. In reality, I did about 10% of the work while one of my best friends did all the hard stuff, but details…

Nothing glamorous. Just a few men, a plan, and a trip to Menards to grab the components needed to get the job done. Breakers, wire, outlets, junction boxes. The usual.

Somewhere between the electrical aisle and standing in the middle of an unfinished garage, it hit me. I didn’t even need to turn things over or flip boxes around. Reading the small print on the back of every component.

MADE IN CHINA.

Every single one.

The breakers that will protect my garage from burning down — made in China. The wire running through the walls — made in China. The outlets I will plug my tools into — made in China. The junction boxes, the lightbulbs. China. China. China.

I stood there in the garage for a moment and thought about what this stuff would cost if it were made in America. Real answer — about three times as much. The electrician I hired to bring my house up to code didn’t charge me three times as much because the parts were already at the house. The parts being cheap is the only reason any of this is remotely affordable for a regular person trying to fix or build a home.

Americans love the idea of Made in America. It polls beautifully. It sounds great on a bumper sticker. It feels righteous to stand in a Home Depot aisle, fighting the urge to pound your chest and look at the flag.

But here is the part nobody wants to say out loud — Americans are not ready for what Made in America actually costs. They are not ready for a $47 outlet. They are not ready for a $180 breaker. They are not ready for construction costs that make today’s housing market look affordable by comparison.

We want the factories back. We want the jobs back. We want supply chain independence. What we do not want is the bill.

And that is the problem, nobody in Washington is honest enough to put on a bumper sticker.

The garage is wired. And somewhere in a factory on the other side of the world, someone worked a 60-hour week to make sure I could afford to do it.

The most interesting things I read this month:

Trump Says Ceasefire With Iran is Over After Latest Attacks

Trump Says Ceasefire With Iran is Over After Latest Attacks —WSJ 7/8/2026

President Trump said he believed his ceasefire deal with Iran was over and that the U.S. would likely carry out more strikes soon, following another round of Iranian attacks on ships in the Strait of Hormuz that snarled efforts to reopen the strategic waterway.

“We hit them very hard last night…probably hit them hard again tonight,” Trump told reporters at a NATO summit in Ankara on Wednesday. “I’ll give them a little warning, we’re going to hit them hard tonight. But we’ll see how it all works out.”

The president’s remarks were the starkest sign yet that diplomacy with Iran has stalled under the preliminary peace agreement he signed in mid-June.

During earlier comments to reporters, sitting next to North Atlantic Treaty Organization Secretary-General Mark Rutte, Trump stopped short of saying the U.S. would restart the war, however, and said he would let talks continue if the parties were willing.

“To me, I think it’s over. I don’t want to deal with them anymore,” Trump said.

“They’re liars, they’re cheats, they’re sick people,” Trump added. “Now I’ll let our wonderful negotiators keep talking if they want, but I don’t see it.”

Trump’s remarks came after the U.S. and Iran traded blows in fighting ignited by Iranian attacks on ships including a liquefied natural gas tanker in recent days. The U.S. military said it hit more than 80 targets primarily along Iran’s coast near the strait, and Iran responded with strikes of its own, launching drones and ballistic missiles at Bahrain and Kuwait, both of which host U.S. military bases.

They’re liars. They’re cheats. They’re sick people.

That is the President of the United States at a NATO summit — sitting next to the Secretary General of the most important military alliance in history — describing the country he signed a ceasefire with three weeks ago. The ceasefire, he called a historic victory. The deal he announced to stop the market from falling apart every time the 10-year Treasury has hit 4.4%.

Words mean nothing in this war. They haven’t since the first bomb dropped.

Here is where we actually are. Iran struck an LNG tanker in the Strait of Hormuz. The US hit more than 80 targets along Iran’s coastline in response on the first night alone. Iran launched drones and ballistic missiles at Bahrain and Kuwait — both hosting American military bases. The Strait remains functionally closed. The ceasefire that was supposed to end all of this is now, in the President’s own words, over. And Trump is telegraphing the next strike to reporters on camera at a NATO summit, as if he were announcing a press conference.

“I’ll give them a little warning; we’re going to hit them hard tonight.”

This is not a strategy. Sounds like desperation dressed up as strength.

The Strategic Petroleum Reserves, meant to cushion the blow of a prolonged energy shock, are depleted. The weekends are for war playbook — the pattern of announcing ceasefires Sunday night and resuming strikes after market close on Friday — has been exposed so many times that markets barely react anymore. Iran knows the timing. Iran knows the Treasury pressure. Iran knows that every announcement of peace is driven by the bond market, not by battlefield calculations. They have been running the same play since February, and it keeps working.

Trump is searching for any leverage that doesn’t exist. Iran struck a US protected LNG tanker not because they miscalculated, but on purpose. They know the US cannot sustain $120 oil indefinitely or even for a few months. They know the Treasury market has a breaking point. They know that Scott Bessent is on the phone with commodity traders every time crude threatens to go parabolic. They know that the American political system cannot tolerate pain for longer than a news cycle.

The markets will continue to be treated as more important than lives. Every ceasefire announcement will be timed to a Treasury auction or a stock market open. Every escalation will be followed by a hint of talks to walk the S&P back from the edge. This is not foreign policy. It is market management with missiles.

Trump said he doesn’t want to deal with them anymore. Iran is counting on that. An adversary who wants to walk away is an adversary who will eventually accept worse terms just to leave. Iran has been waiting four months for America to get tired.

IRAN IS NOT TIRED. THIS IS THE MOMENT IRAN HAS BEEN WAITING FOR, FOR 40 YEARS.

The ceasefire is over, and the world's most powerful military is announcing its next strike to a room full of journalists.

That does not sound like winning.

Lag 7

For years the Magnificent Seven (Mag 7) were the greatest cash generating machines Wall Street had ever seen. They bought back their own shares by the billions — borrowing cheap money at near zero interest rates to reduce share counts, inflate earnings per share, and send their stock prices to levels that made the dot com bubble look like a warmup act. It was the greatest financial engineering story of a generation.

That story is over.

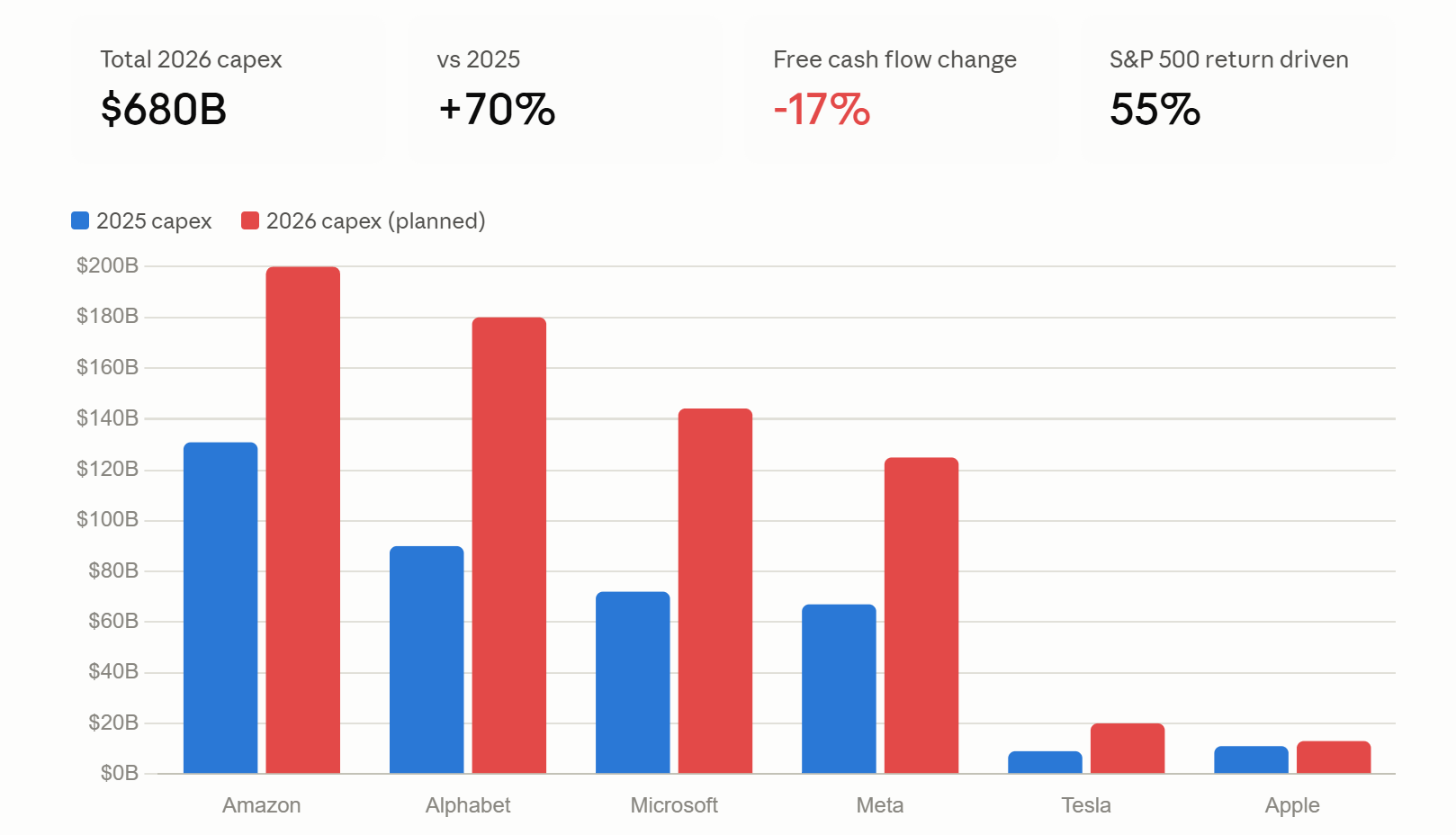

The same companies that spent a decade vacuuming up their own shares are now issuing new ones. The cash that once flowed back to shareholders is now flowing into data centers, GPUs, and AI infrastructure at a scale that would have seemed delusional five years ago. The Magnificent Seven are collectively planning to spend over $680 billion on capital expenditures in 2026 alone. That is up from roughly $400 billion in 2025. A 70% increase in one year.

Let that number sit for a moment. $680 billion. In a single year. With Iranian missiles hitting the Middle Eastern data centers they need to build in, a domestic grid too underpowered to support them, and a return on investment timeline that nobody can honestly define.

Alphabet guided 2026 capital expenditure of $175 to $185 billion — more than double its 2025 outlay. Amazon forecasts $200 billion in capex, up 53% from last year and well above Wall Street’s estimate of $145 billion. Meta is spending $125 billion. Microsoft is on pace for $144 billion.

The free cash flow that made these companies the darlings of every index fund in America is shrinking fast. Capital expenditure across the six that have reported surged 75% year over year to $136.6 billion for the quarter. As a result, free cash flow fell by more than a sixth year over year.

They are becoming cash broke in the pursuit of AI dominance. And here is the part that should make every investor uncomfortable — nobody can tell you with a straight face what the return on that investment looks like or when it arrives.

Microsoft reported 15 million paying Copilot customers for its AI assistant, which sounds impressive until you realize that is a fraction of its 450 million Microsoft 365 customer base. Investors were not impressed. The stock was crushed. The market is starting to ask a question these companies do not have a clean answer to: when does the spending become profit?

The Magnificent Seven accounted for 55% of the S&P 500's total return from 2023 through 2025. But that weighting can work against them in downturns. Since they make up such a large part of the major indexes, dragging the rest of the market down is also a possibility.

One third of the American stock market. Spending money it used to return to shareholders. Into an AI buildout with no guaranteed return. At valuations that assume everything goes right. That is scary.

This is the setup nobody on CNBC is connecting plainly. The companies that propped up the market through COVID, through rate hikes, through Liberation Day — are now making the biggest and most uncertain capital bet in corporate history. Simultaneously. At the top of the market.

The Magnificent Seven spent years buying back shares with borrowed money to look rich. Now they are issuing shares and spending cash to actually become something new. Maybe it works. AI may well be the most transformative technology in human history, and the returns could dwarf the investment.

But maybe it doesn’t. And if it doesn’t, the companies that hold up a third of the American stock market will have burned through the cash cushion that made them bulletproof — right when the world needs them to be.

Stock Indexes Are Divided on Rules for Megacap IPOs. How Exposed Will You Be?

Stock Indexes Are Divided on Rules for Megacap IPOs. How Exposed Will You Be? —WSJ 6/5/2026

The rules are changing for IPOs, and not for the better.

Advisers for SpaceX reached out to major index providers to discuss how it and other hot startups might join key indexes sooner than normal, The Wall Street Journal reported earlier this year. Inclusion in major indexes can significantly boost demand for a company’s shares from institutional asset managers that must buy in order to track their benchmarks.

Faster inclusion also helps indexes accurately track the universe of public companies, and means index-fund investors will have exposure to some of the biggest and hottest newly public companies faster than they otherwise would have. If your goal in owning a large-cap index fund is to be invested in all of the biggest U.S. firms, new fast-tracking rules help accomplish that sooner.

SpaceX is expected to go public at an extremely expensive valuation based on metrics like price-to-revenue, and skeptics aren’t excited about rule changes that could put the company into millions of Americans’ retirement plans sooner.

Some say that allowing a company like SpaceX into an index soon after it starts trading mostly benefits early investors in the company, by allowing them to easily sell their stakes.

But S&P’s move to keep profitability requirements avoids the most controversial issue, and maintains existing criteria for the most-popular U.S. index. Other indexes that simply include the largest companies argue that they are adding fast-tracking rules so they can accurately track the market sooner.

When the game isn’t going the way you want, you have two choices. You can play better. Or you can change the rules.

Nasdaq just changed the rules.

To accommodate the anticipated IPOs of SpaceX, Anthropic, and OpenAI, Nasdaq has quietly loosened its listing requirements. The official reason is modernization. The real reason is desperation. The AI bubble needs new fuel, and the world's most valuable private companies need an exit for their early investors. Nasdaq just handed them one.

Let’s be clear about who benefits from this and who doesn’t.

Who Benefits? Early investors — the venture capital firms, the insiders, the employees sitting on stock options worth more than most people will earn in a lifetime will benefit enormously. The moment these companies hit public markets at peak valuations, the people who got in early get the long awaited cash. They get to sell. They get to leave.

You get to buy.

And here is the part that should make every passive investor’s stomach turn — whether you plan to buy SpaceX, Anthropic, or OpenAI or not, you will. The moment these companies hit the major indexes, every index fund, every 401k, every passive Nasdaq tracker automatically owns them. You don’t get a vote. You don’t get a choice. You are being forced to buy some of the most expensive companies in financial market history at valuations with no historical precedent.

SpaceX was recently valued at 100 times sales. ONE HUNDRED TIMES SALES. That number wasn’t even seen at the very peak of the dotcom bubble — right before the Nasdaq lost 80% of its value over the following two years.

The rules Nasdaq loosened existed for a reason. Listing requirements are not bureaucratic red tape. They are risk filters. They exist to protect the people on the other end of the trade — the retail investors, the pension funds, the ordinary people whose retirement accounts don’t have a venture capital team doing due diligence on their behalf. Loosening those filters doesn’t reduce risk. It transfers it. From the insiders who are selling to the public who is buying.

The WSJ noted it plainly — some say that allowing a company like SpaceX into an index soon after it starts trading mostly benefits early investors by making it easier to sell their stakes. That is the cleanest summary of what is actually happening here.

The S&P 500 held firm and did not follow Nasdaq’s lead. That is worth noting. When the most important index in the world declines to bend its rules for the hottest companies on the planet. That is a signal.

The market is not valuing these companies. It is feeding the monster.

Kevin Warsh Wants the Fed to Stop Explaining Everything

Kevin Warsh Wants the Fed to Stop Explaining Everything — WSJ 6/14/2026

The Old Gentleman’s Club just got new management. The new Fed Chair, Kevin Warsh, has arrived and already begun to put his spin on things.

Kevin Warsh boiled down his advice for the Federal Reserve before an audience of investors last year. “Stop talking so much,” he said. “More thinking, less talking.”

For more than a decade, Warsh has argued that the Fed should say less. How much a central bank reveals about its thinking shapes mortgage rates, markets and the cost of borrowing for everyone.

In Warsh’s view, the central bank has buried itself in its own communication. It produces forecasts that markets fixate on and that box the committee in. Officials give speeches or interviews on every side of every question. Warsh wants the Fed to say less and let markets do more of the work.

The Federal Reserve has operated the same way for 100 years. Press conferences after every meeting. Forward guidance carefully wordsmithed to move markets a quarter point at a time. The result is a central bank that spends more time managing its own narrative than managing the economy.

Warsh just ended that era.

His four task forces will gut and rebuild the central banking platform from the inside. Communication — how the Fed talks to markets. Balance sheet — what the Fed holds and why. Economic data — what the Fed measures and how. Productivity, jobs, and the impact of AI — something no previous Fed Chair has ever formally tackled. And inflation framework — the foundation every interest rate decision is built on.

That is not a tweak. That is a renovation.

The old gentlemen’s club ran on consensus, comfort, and the unspoken agreement that nothing would change too fast. Warsh is a different animal. He has been arguing for a decade that forward guidance — the Fed’s practice of telegraphing its next moves to markets — has turned the central bank into a hostage of its own words. When you tell markets what you are going to do, you have to do it. You lose the flexibility that makes monetary policy effective in the first place.

Saying less gives the Fed its power back.

Now, here is the political reality underneath all of this. Trump put Warsh in this chair for one primary reason — to lower interest rates. Cheaper money means easier borrowing, a higher stock market, and a war economy that doesn’t immediately bankrupt the Treasury. The problem is the Fed committee is currently leaning toward hiking rates, not cutting them. And the Fed Chair cannot move rates alone. The committee votes. Warsh can modernize the communication strategy, rebuild the balance sheet framework, and study the impact of AI on jobs all he wants — but if the committee votes to hike, rates go up regardless of who sits in the chair.

Trump Picked Warsh to Cut Rates. His Committee Is Talking About Hikes. — WSJ 6/16/2026

When President Trump picked Warsh in January, the Fed looked headed for lower rates—and the cheaper mortgages and loans that come with them. Investors expected several cuts this year, on top of three in late 2025, thanks in part to a wobbly job market that left officials worried that high rates were doing more harm than good. Inflation, meanwhile, looked like it might resume a decline toward the Fed’s 2% goal once the effects of tariffs faded.

Four months later, almost none of that holds. Hiring has picked back up, and inflation is climbing instead of cooling. It’s now running above 3%.

The forces behind the turn weren’t the ones the Fed had braced for. The AI build-out, once expected to tame inflation by lifting productivity, instead looks like a source of it—straining supplies of chips, electricity and the materials to build data centers in a way that smacks of a boom rather than a slump. Soaring tech stocks are adding fuel, leaving investors feeling flush and spending freely.

And the war Trump launched in Iran sent gasoline and commodity prices higher. A deal to reopen the Strait of Hormuz will ease pressures, but slowly, and the economy that emerges won’t be the one that existed before the war. The case for cuts has gone with it.

Trump may have installed his guy. His guy may still have to deliver news Trump doesn’t want to hear.

The era of the Fed telling you exactly what it is going to do before it does it is over. Whether that means lower rates or higher ones, markets will have to do something they have forgotten how to do.

Think for themselves.

GM in Talks to Supply Weapons Parts to Lockheed Martin

GM in Talks to Supply Weapons Parts to Lockheed Martin — WSJ 6/16/2026

GM, back in the weapons business, tells you everything you need to know about the true levels of US munitions supplies.

General Motors is in talks with Lockheed Martin about making parts for the defense contractor’s weapons, according to people familiar with the matter.

Under the arrangement, GM would manufacture commonly used parts that could help Lockheed bolster munitions production, the people said. The companies are discussing which components GM could potentially make.

“Today’s environment requires us to think differently about how we strengthen the industrial base,” Lockheed Chief Operating Officer Frank St. John said. “Production capacity is a national security capability.”

Pentagon officials have said they might need the companies to backstop traditional defense contractors that are struggling to meet demand for strike weapons and interceptors that the U.S. and its allies burned through in the Middle East this year.

Read that last line again. The Pentagon needs General Motors to backstop traditional defense contractors that are struggling to meet demand. The company that builds your truck is being called in to help the company that builds missile defense systems because the missile defense company cannot keep up.

Ask yourself when exactly America decided the company that builds your truck should stop building the weapons that defend your country. The answer is the same answer it always is. It was cheaper not to.

During World War II, American manufacturing was the arsenal of democracy. GM wasn’t building Chevrolets. Ford wasn’t building Mustangs. The entire industrial base of the United States was converted overnight into the most prolific weapons manufacturing operation the world had ever seen. Tanks, planes, ships, and ammunition poured out of American factories at a pace that genuinely changed the outcome of the war.

Then the war ended. And over the next 70 years, in the name of efficiency, shareholder returns, and the relentless pursuit of cheaper, America quietly dismantled that capability and handed it to the lowest bidder.

Now we are paying for it.

Stocks of critical weaponry have been depleted by two simultaneous wars — Iran and Ukraine — with no credible plan for replenishment. The official position from Pete Hegseth and the Trump administration is that American munitions stockpiles are ample and the situation is under control.

So explain this.

If stockpiles are ample, why did the US pull THAAD missile defense systems out of Asia in what can only be described as desperation? THAAD is the system protecting Taiwan, Japan, and South Korea from North Korean and Chinese ballistic missiles. Removing it leaves China with an open window on Taiwan and leaves our two strongest allies in the Pacific — the same countries we need to reshore our supply chains and buy our Treasuries — with zero protection. You don’t pull your most advanced missile defense system from the most strategically sensitive region on the planet because you have plenty of everything.

If stockpiles are ample, why is the Pentagon calling General Motors?

The math is simple and brutal. At current production rates, we are looking at three to four years to replenish what has been spent. Three to four years during which China, Russia, Iran, and North Korea are not taking a break.

And here is the part nobody in Washington wants to say out loud. Bringing this manufacturing back to America is the right call. It is also going to be extraordinarily expensive. American labor costs more than foreign labor. American environmental standards cost more than no standards. American supply chains cost more than Chinese ones. Every shell casing, every guidance system, every component that gets reshored adds to the bill.

Rebuilding the arsenal of democracy in 2026 will be inflationary. There is no version of this that isn’t. The question is whether America is willing to pay the price of being able to defend itself, or whether we keep choosing cheaper until cheaper gets someone killed.

GM building weapons parts again isn’t a feel good story about American manufacturing. It’s an admission that we let something critically important slip away in the name of a margin.

Cheaper isn’t always better. Sometimes it’s just cheaper until it isn’t.

Rocked by the Iran War, the UAE sours on Trump

Rocked by the Iran War, the UAE sours on Trump — The Washington Post 6/24/2026

The United Arab Emirates just sent Washington a message. They are done pretending this war was a success.

The UAE — America’s most reliable partner in the Gulf, the country that hosts US military bases, the country that has quietly enabled American power projection across the Middle East for three decades, is turning sour on Trump over the Iran war. And if the UAE is willing to say it out loud, you can be certain every other Gulf state is thinking it behind closed doors.

But the UAE isn’t the most interesting defection this month.

The neocons are turning too.

The neoconservatives who have pushed regime change in Iran since the Reagan administration — the think tank architects, the foreign policy lifers, the people who have spent 40 years arguing that one more strike, one more sanction, one more push would finally topple the Iranian government are quietly stepping back from the war they spent decades demanding. The public defeat Trump wanted them to suffer is beginning to materialize.

We said this in the April letter. Our base case since the beginning has been that the Iran war would serve as the mechanism for breaking up the structural dependency between the United States and Israel — and for finally discrediting the neoconservative foreign policy apparatus that has driven America into the Middle East repeatedly for 40 years. Not through a policy paper. Not through a congressional debate. Through exposure. Let them have their war. Let the world watch what it costs. Let the American public see whose idea this was.

Like a moth drawn to a flame, the only way to stop the moth is to let it reach the flame. Trump may be closing in on simultaneously discrediting the neocons who want America in permanent war, redefining the toxic dependency on Israel, degrading Iran’s nuclear capability, and rebuilding American energy dominance from scratch. If he pulls it off, it would be the biggest presidential win since WWII.

If this conclusion is even remotely correct, there will be no TACO. The neocons and Netanyahu are going to suffer a painful and public defeat. Trump has the Western media exactly where he wants them — broadcasting that this was Israel’s idea, that Trump was duped, that the war was Netanyahu’s war. Whether entirely true or not, half the country believes what MSNBC reports, and the other half believes Fox News. Either way, the narrative is being shaped.

The Israeli Times reported it. Vance made the call to Netanyahu. The Western media ran with it. Netanyahu oversold regime change. Trump went along. The war didn’t end in two weeks. The Strait is still closed. The Treasury market is fragile. It’s beginning to make more sense now why the UAE threatened that either they get a swap line, or energy will be priced in Chinese yuan moving forward.

The neocons got their war. They are not getting their victory.

When the people who wanted this war the most stop defending it, the war is lost. Not on the battlefield. In the minds of the people who funded it, planned it, and sold it to three consecutive American presidents.

That is how the war in Iran actually ends.

For 50 years, the petrodollar system has run on a simple arrangement. Gulf nations sell oil in dollars, recycle those dollars into US Treasury bonds, and America gets cheap oil and a permanent buyer for its debt. That arrangement is now cracking.

The Gulf states are watching the Iran war destroy their neighbors’ energy infrastructure, close the waterway their entire economy depends on, and expose the American security guarantee as conditional and unreliable. The petrodollar surplus that used to flow automatically into Treasury auctions is being consumed by a war nobody in the Gulf asked for. The UAE is demanding a swap line or risk dollar dominance. Others are quietly redirecting surplus eastward toward China.

The United States needs buyers for its debt more urgently than at any point in modern history — and the most loyal buyers in the room are leaving. You find out what American debt is actually worth when that happens.

Lifestyle

Budgeting

"Now let me leave this little word of counsel for you. Keep a little ledger, as I did. Write down in it what you receive, and do not be ashamed to write down what you pay away. Write down every single item." —JD Rockefeller

J.D. Rockefeller would go so far as to reward his child who kept the most accurate expense ledger.

I started tracking every dollar I spend a few months ago. Not because I was in trouble. Because I realized I didn’t know 100% where my money was actually going, and that bothered me more than whatever the number turned out to be.

The mortgage I knew. The insurance, the utilities, and the gym membership. What I didn’t know was everything in between. The dinners that add up to a car payment. The subscriptions quietly renewing in the background. The hundred small decisions that happen on autopilot between paydays that consume more than you think it should.

When I finally sat down and looked at it honestly, it was slightly uncomfortable. That discomfort was the point.

You cannot improve something you don’t track. I have said that in this newsletter before. It applies just as much to your bank account. The simple act of writing down where your money goes forces a confrontation with reality that most people spend their entire lives avoiding. And that confrontation is where things actually get better.

Budgeting does three things at once. It reduces stress — because uncertainty is always scarier than the actual number. It shows you exactly where your money is going, so you can make deliberate choices rather than reactive ones. And it builds the habit of treating your personal finances the way a good business treats its books. With accountability. With intention. With a clear picture of what is coming in and what is going out.

The tools don’t matter. I use a simple spreadsheet on Google Sheets since it’s free. A notebook works. An app works. Whatever you consistently open is the right answer. What matters is starting. Pick a month. Track everything. At the end of thirty days, you will know more about your financial life than most people learn in a decade.

We are living in an inflationary world where the cost of everything is going up, and the purchasing power of every dollar is going down. In that environment, the people who know exactly where their money goes will be the ones who have money left when it matters most. If your finances are stretched thin right now, this is step one to fixing the issue.

Start this month. You won’t regret it.

Investments

The stock market is the most expensive it has ever been by every measure. Price to earnings. Price to sales. Market cap to GDP. Pick your metric — they all tell the same story. We are at valuations never seen before in modern history, not even the peak of the dotcom bubble in 2000. And we all know how that ended. The difference this time is the world outside the stock market is actively on fire while the market pretends otherwise.

Look at everything covered in this newsletter and ask yourself one question — is any of it deflationary? The Iran war. The Strait closure. Rebuilding 40 years of dismantled manufacturing. Reshoring the defense industrial base. Funding an AI buildout larger than the Manhattan Project, the railroads, and the fiber buildout combined. Universal basic income to replace jobs lost to automation. All of it requires massive money printing into record debt levels just to maintain the status quo. The buyers of that debt are getting nervous. The Treasury market needs more buyers than ever and has fewer than ever. That is not a backdrop that ends with a soft landing.

I am positioning accordingly. Most of my new money is going into gold and Bitcoin to combat the coming inflation, whether markets have priced it in or not. I am limiting my exposure to the Magnificent Seven as much as possible — the companies propping up a third of the S&P are burning cash into an AI bet with no guaranteed return, sitting in a market priced for perfection, and the world is not a perfect place. Many of these stocks are at the lowest prices in over a year. One development from China could crash this market. You may underperform the market for a year or two, taking this posture. A lost decade or worse is coming for those who don’t. This AI buildout has no finish line and no guaranteed winner. Position like it.

401k

Small change to allocation.

33% International Small Cap Value

33% Diversified International Fund

33% Change from S&P 500 Index to Vanguard Growth Index Fund

Small change to the 401k this month. I used AI to backtest every fund option available in my plan against the S&P 500, going back as far as the data allowed. The Vanguard Growth Fund was the only option that barely beat it. So I made the switch. A few extra percentage points of return, compounded over decades, can make a difference.

Most people set their 401k allocation once and never look at it again. I have been guilty of this too. The reality is your 401k is likely your largest investment vehicle and it deserves the same attention you give everything else. The tools for this analysis are now available to everyone now. Pull up your plan options, feed them into an AI, ask it to backtest performance against the S&P 500, and see what comes back. It takes thirty minutes, and the results might surprise you.

I am still bullish on international equities on the reshoring thesis — South Korea and Japan remain my conviction plays for when America needs its Asian allies to rebuild its industrial base. That allocation stays. Plus, not being in high-risk American markets has short-term benefits. The switch from a broad index to the Vanguard Growth Fund is a small tweak with a meaningful, very long-term impact.

Bitcoin MSTR 0.00%↑ MSBT 0.00%↑

Bitcoin is cheap. Not cheap in the way a failing business is cheap — cheap in the way an asset gets cheap when the world is distracted by a war, and nobody is paying attention to the underlying thesis. The underlying thesis has not changed. If anything, it has strengthened every single month this newsletter has been written.

Trump and Bessent can walk back dollar debasement talks all they want. The talks were walked back because markets needed calming, not because the problem was solved. The debt is still there, and the deficit is still blowing out. The Treasury market still needs more buyers than it has. The petrodollar recycling mechanism is still cracking. The printing press is still the only tool left when everything else fails. Bitcoin was built for exactly this environment — and capital will flow into it when the world catches up to what is already happening. That takes time. It always does.

I added Morgan Stanley Bitcoin Trust MSBT 0.00%↑ to my Bitcoin holdings this month as another way to ride the thesis. MSBT 0.00%↑ has a net asset value (NAV) of $18.27 per share and trades at a discount on most days. The expense ratio is cheap at 0.14%. I am still dollar cost averaging every week through the River app and have no intention of stopping. I will double my weekly position before I stop buying. The position is sized for a long timeline. The world will need a non-sovereign store of value before this decade is over. Bitcoin is the only candidate that has survived long enough to be taken seriously, and can be sent in a timely manner.

Gold AU 0.00%↑ B 0.00%↑

Central Banks Are Rethinking Where They Store Their Gold —WSJ 6/16/2026

Central banks are increasingly shifting where they store their gold—a move that reflects growing geopolitical concerns and a desire to ensure greater control and access to reserves.

A survey from the World Gold Council, an industry body representing gold miners, showed fewer central banks now store bullion in London and New York than a year earlier, two hubs that house the world’s most liquid bullion markets.

“This year’s survey reveals an emergent trend of central banks increasingly looking to diversify gold vaulting locations,” the WGC said Tuesday.

Central banks do not repatriate gold in times of peace and prosperity. They repatriate gold when they are preparing for something.

Think about what it means to move your gold out of London and New York — the two most liquid bullion markets in the world. You are accepting less liquidity, higher storage costs, and greater logistical complexity. Nobody does that without a reason. The reason is that London and New York are American and British — and after watching Russian reserves frozen overnight in 2022, every central bank on the planet quietly asked itself the same question. What happens to our gold if we end up on the wrong side of Washington?

The answer was to bring it home or send it somewhere safer.

Now ask the next question — if gold isn’t going to play a larger role in the global financial system, why does it matter where it’s stored? It matters because the countries moving their gold are positioning for a world in which gold is not just a reserve asset but also an active settlement tool. We are already watching this in real time. Iran accepting gold for tanker tolls. Countries selling gold to China for yuan to pay for oil. China opening gold exchanges across the world to make the metal more accessible as a trade settlement mechanism. This is not speculation. It is happening in the headlines of this newsletter every single month.

Trump and Bessent are helping China’s gold strategy by driving down the price of gold versus the USD. Every time the dollar strengthens, dollar-priced gold goes down — and China, which has been accumulating gold at a pace that nobody in the West can accurately measure, pays less for every additional ounce. And China is fine with playing the long game. I will not stop buying gold until China does. And China is not stopping.

PBF Energy PBF 0.00%↑

No change in stock holdings.

We now know how Trump was actively manipulating the price of oil during the Iran War. And it’s worse than you expected.

Trump secretly approved Qatar-Iran cash deal — 6/15/2026

The US secretly approved a financial and maritime arrangement between Qatar and Iran, under which billions of dollars were paid to Tehran in exchange for free passage for Qatari tankers and ships through the Strait of Hormuz, three diplomatic officials now confirm.

This was a deliberate and conscious course of action by the US administration, which allowed its navy to turn a blind eye to the arrangement, in complete contradiction of its declared policy. The move was intended to ease the crisis in global energy markets and curb rising oil prices.

The current revelation proves that the White House had already laid the groundwork at the time for the memorandum of understanding being forged with Iran. In doing so, the administration gave Iranian terrorism a critical economic lifeline at a moment of particularly severe financial strangulation.

Let that sink in.

The United States Navy was enforcing a naval blockade of Iran. American sailors were putting their lives on the line to strangle Iranian oil revenues and force a negotiated end to the war. While that was happening, the Trump administration was secretly approving Qatar to pay Iran billions of dollars to let oil through the same Strait the Navy was blockading.

The left hand was enforcing the blockade. The right hand was paying to break it.

This is why oil never made sense during the war. Bad news sent oil up 5%. Good news sent it down 13%. The Financial Times reported that Bessent was on the phone with large commodity traders. Now we know the full picture. It was not just market communication. The administration was actively managing the physical oil supply behind the scenes while publicly declaring a naval blockade. The price of oil was being managed from both ends simultaneously — suppressed through secret payments to Iran and manipulated through back channels with Wall Street traders.

The US Navy publicly blockaded Iran. Trump paid Iran to open the Strait in private. The sailors enforcing the blockade had no idea the deal was already being cut above their heads.

That is not foreign policy. That is a betrayal of every service member who was put in harm’s way under the pretense of a nonexistent strategy.

Iran got its economic lifeline at the moment of maximum financial pressure. The moment when the sanctions and the blockade were working. The moment when a little more patience might have produced a real result. Instead, the administration blinked — secretly, so nobody would notice, and handed Tehran exactly what it needed to keep fighting.

Trump gave Iran a lifeline to stabilize its stock market. The Navy paid the price for it.

PBF remains a hold. The energy crisis is not over. Infrastructure destroyed during the war will take years to rebuild, regardless of what any deal says on paper. Crack spreads remain favorable, and jet fuel shortages are not resolved by a secret payment from Qatar. The thesis is intact.

Sirius XM SIRI 0.00%↑

No change in the position after trimming some last month.

Sirius is having a good year, and I don’t expect that to change.

SiriusXM’s first-quarter results showed free cash flow tripling year over year, churn falling to a record-low 1.5%, and EBITDA margin expanding, prompting management to reaffirm robust full-year guidance of roughly $8.5 billion in revenues, $2.6 billion in adjusted EBITDA, and $1.35 billion in free cash flow.

Growth catalysts are building: April’s exclusive YouTube audio-advertising partnership extends reach toward 255 million monthly listeners starting this fall, while May’s expanded LiveRamp identity-targeting deal with AdsWizz strengthens programmatic monetization. June’s video-podcast distribution agreement with Tubi adds 100 million monthly users, leveraging podcasting’s strong revenue momentum. With leverage trending toward management’s low-to-mid 3x target and continued capital returns, this Zacks Rank #3 company’s broadening advertising ecosystem and disciplined execution support a constructive near-term outlook.

The Zacks Consensus Estimate for 2026 earnings has remained steady at $3.10 per share in the past 60 days. In the past six-month period, SIRI shares have returned 35.8%.

—Zacks Industry Outlook

Alibaba BABA 0.00%↑

Sold!

I sold my stake in Alibaba this month. After five years of owning it, I needed a break — and more importantly, the thesis changed.

Alibaba is the Google of China. It is one of the most dominant technology companies on the planet, a genuine leader in AI, and by almost every fundamental measure, it is cheap. None of that matters right now. What matters is that Trump and Bessent have made it abundantly clear they will not allow Chinese companies to win the AI war. The Pentagon labeled Alibaba an aid to the Chinese military. Export controls are tightening. The geopolitical environment between the US and China is not improving — and in that environment, owning the most visible Chinese AI company is owning a target.

I will be looking to reenter at some point. The business is too good, and the valuation is too cheap to ignore forever. But after five years of watching this stock fight through trade wars, delisting threats, regulatory crackdowns, and now an active shooting war that has redrawn the lines between American and Chinese interests — I am taking the break it has earned me. Sometimes the best investment decision is the one that lets you sleep at night.

New Position: Tencent Music Entertainment TME 0.00%↑

I opened a new position in Tencent Music Entertainment this month. TME is the dominant music streaming platform in China — think Spotify, but for 1.4 billion people — and it is trading at roughly one-tenth of Spotify's valuation. That kind of discount does not exist without a reason, but in this case, the reason is geopolitics, not fundamentals. And geopolitical discounts on great businesses are historically where the best returns come from.

The financials are genuinely impressive. TME is profitable, growing, and throws off real cash. It is a spinoff of Tencent, one of the most sophisticated technology conglomerates in the world, which means its operational DNA and balance-sheet discipline are in place. The music streaming business in China is still in its early innings compared to Western markets, where streaming penetration is mature. TME has room to grow into its valuation in ways Spotify simply does not at current prices.

The risk is the same as on every Chinese equity right now — geopolitics. I sold Alibaba partly because the target on its back had gotten too large. TME is a different profile. It is a consumer entertainment company, not an AI infrastructure play. It is not on the Pentagon’s radar. It does not compete directly with American technology interests. For a Chinese equity in this environment, that distinction matters. I am sizing this position accordingly — meaningful but not oversized — and will add if the thesis continues to develop.

This is part of getting back to the basics as an investor. This has legitimate 10x potential, unlike Alibaba.

Nam Tai Properties $NTPIF

Nam Tai has been quietly gaining momentum, and the next 60 days will tell us everything about whether that momentum is real or just noise. Three catalysts are on the clock simultaneously, and the stock cannot afford to miss any.

First, the press release announcing the new technology center must come before July 30th. That announcement has been dangled long enough that the market has partially priced it in — which means a delay hurts more than an on-time delivery helps. Second, Q2 earnings hit August 14th and the technology center has to show up in the numbers in a meaningful way. A press release without financial proof is just a press release. Third, the annual meeting came and went with no news on relisting. That silence is not fatal, but it is not encouraging. The relisting was supposed to be the catalyst that unlocked this position. Every quarter it gets pushed further the thesis gets harder to hold.

I am still holding but watching closely. Nam Tai has been a lesson in patience that has tested every definition of the word. The business is real, the assets are real, and the Shenzhen technology hub location is genuinely valuable. But real assets need real catalysts to move a stock — and July 30th is the next moment of truth. Miss it, and this position gets a serious reassessment.

GameStop GME 0.00%↑

Ryan Cohen is going after eBay, and I believe he will figure out a way to get it done.

Cohen has been aggressive and public about the pursuit, making it clear this is not a casual conversation. Michael Burry reiterated this month that a GameStop acquisition of eBay would create an instant Berkshire Hathaway — a cash generating machine with a built in marketplace, a loyal customer base, and a CEO who has already proven he can take a dying retail brand and turn it into something the market underestimates. That thesis is compelling enough that I am staying in the position despite the one thing that gave me pause this month.

GameStop approved a share count increase, and I do not love it. Dilution is dilution and shareholders deserve a straight answer about what those shares are for. The most charitable read is that Cohen needs the ammunition to fund the eBay acquisition and is positioning the balance sheet accordingly. The less charitable read is that the stock is being used as currency at a moment when the valuation may not justify it. Cohen has earned enough of my trust to get the benefit of the doubt — but this is the kind of move that needs to pay off quickly. If the eBay deal gets done at a price that makes sense, the share increase will be forgiven. If it doesn’t, it won’t be forgotten.

House

Nothing crazy this month. The garage is finally wired — one of the bigger items on the list since we moved in and a project that took longer than it should have thanks to the electrician shortage I mentioned last month. Walking out there and flipping a switch that actually does something is a better feeling than it has any right to be. The closet is almost done as well. What started as a straightforward build has turned into one of those projects that reveals three new problems for every one you solve. We are close enough to the finish line that I can see it.

Spring delivered on its promise. Green grass, longer days, and enough warmth to actually enjoy being outside after a winter that wore out its welcome sometime around February. The trees are in the ground, the garden is planted and being negotiated with the deer on a daily basis, and the house is starting to feel less like a project and more like a home. Better times are here.

That is all for this month. Happy belated 4th of July to my American friends. I can’t believe summer is more than half over.

Thanks for being a part of this!

Casey Donaldson

Disclosure

The investment positions, opinions, and analysis contained in The Rover are for informational and entertainment purposes only and do not constitute financial advice, investment recommendations, or an offer to buy or sell any security. I am not a licensed financial advisor, broker, or investment professional.

All investments carry risk, including the potential loss of principal. Past performance is not indicative of future results. The positions I hold and discuss in this newsletter — including but not limited to Bitcoin, gold, PBF Energy, MicroStrategy, MSBT, Sirius XM, Tencent Music Entertainment, Nam Tai Properties, GameStop, Sprott Physical Uranium Trust, and any other securities mentioned — reflect my personal investment decisions and are not recommendations for others to follow.

The Rover may discuss speculative investments, emerging markets, cryptocurrency, and other high risk assets. These are not suitable for all investors. Before making any investment decision, you should conduct your own research, consult with a licensed financial professional, and consider your own financial situation, risk tolerance, and investment objectives.

The information in this newsletter is believed to be accurate at the time of writing but may become outdated. Markets move fast. The world moves faster. Neither The Rover nor its author assumes any liability for decisions made based on the content of this publication.

Invest at your own risk. Think for yourself.